This is the 8th in a series going back to January 2013. Each article chronicles FEMA/political and rate change activities associated with the mercurial matter of rational, fair and solvent flood zones and insurance rates for Key West and the Florida Keys. In early May, the FEMA team was in Key West and provided updated mapping information in an open forum at the Harvey Government Building. There were three critical pieces of information delivered. The first was the greater inclusion of "inland storm surge" into mapping and flood zone designations. Second, was the strong likelihood of at least a 1' and possibly 2' increases in the existing flood zone structure. Third, rate Grandfathering. Let's review -

Background

My first seven blogs have covered legislative efforts to primarily refund the National Flood Insurance Program (NFIP) which, despite these efforts, remains approximately $25B in debt. A quick recap of these seven blogs is:

- Is Your Flood Insurance Going Up - Part VII (August 2017) - Review of the new, bipartisan Senate bill called "The Sustainable, Affordable, Fair and Efficient National Flood Insurance Program Reauthorization Act (SAFE NFIP) 2017.

- Is your Flood Insurance Going Up - Part VI (June 2016) - Update of the FEMA RiskMap mapping project begun in 2013.

- Is Your Flood Insurance Going Up - Part V (July 2014) - Details of the FEMA mapping effort for the Keys and South Florida including an extensive Outreach Program.

- Is Your Flood Insurance Going Up - Part IV (March 2014) - Recap of the March 2014 Homeowners Flood Insurance Affordability Act (HFIAA).

- Is Your Flood Insurance Going Up - Part III (October 2013) - Realization by politicians, including a co-author of flood insurance legislation called the Biggerts Waters Insurance Reform Act of 2012 (BW-12), that BW-12 was causing the consumer more harm than good, aka "unintended consequences".

- Is Your Flood Insurance Going Up - Part II (September 2013) - Treatment of historic buildings, second homes, businesses and no more exemptions under BW-12.

- Is Your Flood Insurance Going Up - Part I (January 2013) - Flood insurance rate changes and their justifications according to BW-12; i.e., refund the bankrupt NFIP.

Inland Storm Surge

FEMA employs a host of modeling systems to predict and address damage assessment. Among the models that speficially address storm surge are:

- TTSURGE and FEMA SURGE are two-dimensional hydrodynamic models used to prepare the detailed hydraulic analyses of the relationship of tropical cyclone storm surge elevations, astronomical tides, shoreline configurations and elevations.

- The Sea Lake and Overland Surges from Hurricanes (SLOSH) model, a two-dimensional hydrodynamic model that predicts coastal and inland storm surge flooding potential at various time intervals.

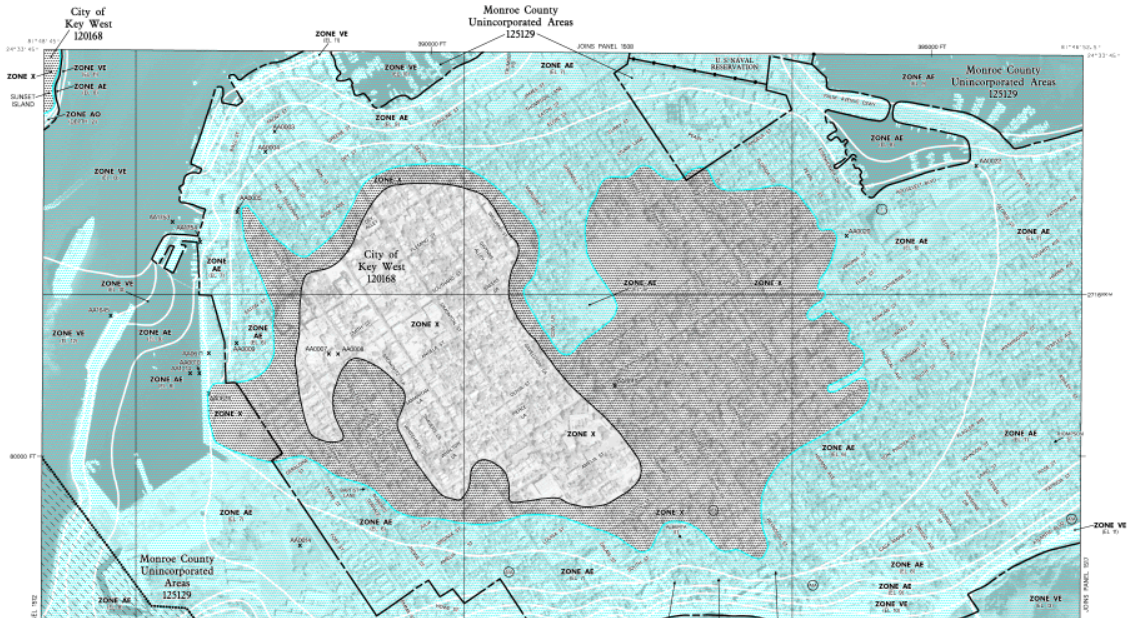

For Key West and the Florida Keys, "inland" is not much more than a mile or two. The lightly undulating topograhy of our island communities means an AE zone could "finger" its way well into the island, even between areas designated as X-Flood zones. In Key West this is apparent as areas around the cemetery, central to the island, are a glove-like patchwork of X and AE Flood zones.

New mapping will likely make these AE fingers fatter, expanding into adjacent X zones, and deeper, AE6's to 7's or 8's.

Flood Mapping

The flood mapping web site I recommend for Key Westers is part of the city of Key West web page and is here. As shown in the Flood Map directly above, there is an inland storm surge AE finger sandwiched between two X-Flood zone areas just west of the cemetery.

I always distinguish the two X-Flood Zones. There is the real X-Flood Zone, above in white, that covers from Eaton Street south to past Truman Avenue and straddles Simonton and Duval Streets. Then there is X-Flood Zone Light, above in grey, that surrounds the real X-Flood Zone. X-Light extends to the East across White Street into the Meadows and east-southeast across Truman Avenue across Old Town - South and towards United Street.

This X-Flood Zone Light, where previously flood insurance has not been required (for mortgage holders), is an area whose perimeter may be changed into an AE rated zone.

Grandfathering

For properties newly mapped into a high-risk zone (e.g., X to AE), some customers will be eligible for a Preferred Risk Policy (PRP). This eligibility exists for two years after the maps change. As long as you have a policy before the end of these two years, policyholders can then “grandfather” the lower-risk zone (e.g., X) to use for future rating. Grandfathering is available for property owners who meet either or these two situations:

- Have flood insurance policies in effect when the new maps become effective and maintain continuous coverage, or

- Built their property in compliance with the Flood Insurance Rate Map (FIRM) at the time of construction

There are some opportunities for homeowners to buy a PRP after the new FIRM maps (which move the property into a higher flood risk zone) come out; however, the surest way for a pre-FIRM property to qualify for grandfathering is to buy or renew a policy BEFORE the new Flood Insurance Rate Map becomes effective. This is true for property owners whose flood zone rating is:

- Moving from a high risk zone into a higher risk zone; i.e. AE6 into AE8, or

- Moving from a non-risk zone into a high risk zone for the first time; i.e. X into AE

Preferred Risk Policy

The Preferred Risk Policy (PRP) is a Standard Flood Insurance Policy (SFIP) that offers low-cost coverage to owners and tenants of eligible buildings located in the moderate-risk B, C, and X Zones in the National Flood Insurance Program (NFIP) Program.

Buildings newly mapped into a high-risk flood area, like from X into AE zones, may be eligible for a lower cost Preferred Risk Policy (PRP) rate in the two years following the map change. Purchasing a PRP BEFORE or during the two year post-mapping period will allow you to retain the lower-risk zone for future rating. Buildings that are newly designated within an Special Flood Hazard Area (SFHA) due to a map revision on or after January 1, 2011, are eligible for a PRP for 2 policy years from the map revision date.

Check with your insurance agent cause this is all way too complicated to not be explained by an expert!!

What if my property is on high ground or built on fill?

For small elevated areas inside a Special Flood Hazard Area (AE zone or higher), FEMA has established two methods to revise the flood designation for that specific property:

- Letter of Map Amendment (LOMA) for properties on naturally high ground

- Letter of Map Revision Based on Fill (LOMR-F) for properties elevated by placement of fill

Letter of Map change information can be found here. NOTE: If you have already submitted and obtained a LOMA or LOMR-F designation and the new flood map changes your flood zone designation, your exemption is no longer valid. But. There is a revalidation process.

Properties that comply with new or modified Base Flood Elevation (BFE) or are located in areas of the community that are not affected by updated flood hazard information can be revalidated through a formal determination letter—called a LOMC Revalidation or LOMC-VALID.

Oh by the way, neither LOMA, LOMR-F nor LOMC-VALID have anything to do with whether or not your area or property has previously flooded or not. It's all about elevation. Click here to see if your property has a Flood Elevation certificate on file with the City. (Type only the name of your Street in the space under Title).

Conclusion

What do I do now?

If you have a flood policy, keep it. If you do not have a flood policy, get one sometime between now and next summer. (New Flood Maps are projected out earliest Fall 2019). Having a flood policy BEFORE the new maps go into effect will benefit you by allowing you to start these premium increases from the lowest possible point. Contact your insurance agent pronto.

Let's face it, if the water is coming up that means flood zones are expanding and premiums are going up. Yes, I am aware of the argument that Floridians pay more in insurance premiums than they receive back in claims. Forget that. Bring in fill, build up, get coverage, play smart.

If you have any comments or questions, please contact me here.

Note: There is a FIRM Fundraiser in Key West on June 1, 2018. Also FIRM Hurricane Readiness & Response Forums on June 12 (Marathon) and June 13 (Big Pine Key).

Thank you to Scott Fraser, FEMA Coordinator, Key West, Mel Montagne, President Board of Directors FIRM and Caroline Horn, Manager FIRM Key West for helping me to write this article.

Good luck!

Additional Resources: